A growing private credit sector, valued at £8.2 trillion, is raising fears of a financial crisis that could rival the 2008 crash, as investors scramble to pull money out of opaque funds. The sector, dominated by firms like Blackstone, Apollo, and BlackRock, has grown rapidly since the 2008 financial crisis, filling the void left by traditional banks that retreated from riskier lending. Now, with signs of a potential implosion emerging, experts warn of a crisis that could spread through the financial system and impact ordinary savers and pensioners.

Private Credit’s Shadow Banking Model

Private credit, often referred to as the ‘shadow banking’ sector, operates outside the traditional financial system by offering loans to unlisted companies that avoid the scrutiny of stock exchanges. Unlike regulated banks, private credit firms do not take deposits from individual savers. Instead, they raise funds from pension funds, insurers, and other institutional investors, which they then lend to private companies in pursuit of high returns.

This model has grown significantly in the years following the 2008 financial crisis. Firms such as BlackRock, Blackstone, and Apollo have become major players in the sector, managing trillions of dollars in private credit. However, the lack of regulatory oversight has raised concerns about the stability of the sector. Unlike traditional banks, private credit firms are not required to maintain capital reserves or adhere to the same lending standards.

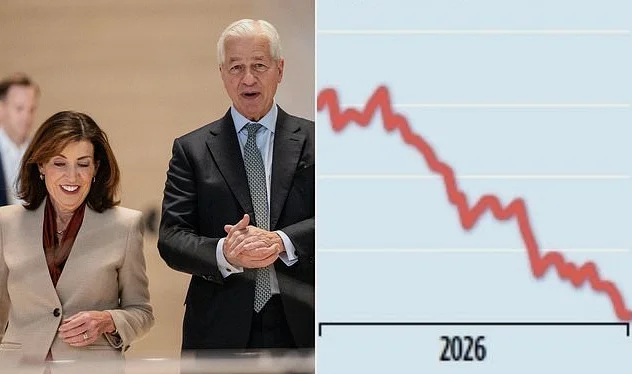

Jamie Dimon, CEO of JP Morgan, the world’s largest bank, has warned that more ‘cockroaches’ will emerge from the financial system, referring to hidden risks and unstable firms. His warning came after the collapse of two major U.S. private credit firms in 2022, which triggered a wave of concern about the sector’s lending practices.

Recent Crises and Liquidity Problems

The recent collapse of Market Financial Solutions, a London-based mortgage broker specializing in property-backed loans, has exacerbated fears of a broader crisis. The firm’s sudden failure left Barclays and Santander with an estimated £1.3 billion shortfall, highlighting the potential ripple effects of private credit defaults.

Following the collapse, major private credit firms have imposed strict withdrawal limits to prevent a mass exodus of capital. BlackRock, the world’s largest asset manager, has limited withdrawals from its flagship private credit fund to 5%, while Blackstone has faced a record £2.8 billion in withdrawal requests. Blue Owl, another major player, has barred investors from accessing funds in one of its retail-focused private credit portfolios.

These restrictions have left investors stuck with illiquid assets, unable to sell their holdings in a timely manner. Unlike traditional stocks, private credit loans are not traded on public exchanges, and the value of these loans is determined by the funds that hold them. Investors can only sell a limited portion of their holdings during specific ‘windows,’ further compounding the problem of liquidity.

Christian Stracke, president of Pimco, a £1.7 trillion asset manager, has warned that the private credit industry is facing a ‘reckoning.’ He described the current situation as a ‘crisis of really bad underwriting,’ pointing to concerns that lending standards have become too lax. The lack of transparency and liquidity in the sector, he said, is a feature, not a bug, of the system.

Comparisons to 2008 and AI Risks

Experts are drawing comparisons between the current private credit crisis and the 2008 sub-prime mortgage crisis. Both involve complex financial structures that obscure who holds the risk, and both involve loans to borrowers that mainstream banks have shunned. However, the private credit market is currently smaller than the sub-prime mortgage market in 2007, and lenders insist that default rates, while rising, remain manageable.

Despite these assurances, the Bank of England has launched its own stress tests to better understand the links between private credit and the broader financial system. This comes after the 2022 crisis, when the Bank was forced to bail out the pensions industry following the Liz Truss mini-budget, which exposed hidden borrowing in workplace retirement schemes.

One potential trigger for the next crisis could be the rise of artificial intelligence. Private credit has heavily invested in the debt of software companies during the tech boom, but AI threatens to upend their business models by automating workflows previously handled by humans using a variety of software services. This could lead to defaults in the private credit sector as the value of these companies declines.

Fergus McCorkell of Troy Asset Management has warned that if investors start to worry about private credit, they may rush to sell their more liquid assets, such as listed equities, first. This could trigger a broader sell-off in financial markets, increasing the risk of a systemic crisis.

The Bank of England has already taken steps to monitor the potential risks posed by private credit. However, the lack of transparency and oversight in the sector means that the full extent of the risks remains unclear. As the situation continues to develop, the question remains: is the private credit sector on the brink of a major collapse, and what could that mean for the global economy?

Comments

No comments yet

Be the first to share your thoughts