QatarEnergy, one of the world’s largest liquefied natural gas (LNG) producers, has suspended operations at key facilities following a series of Iranian military strikes that targeted energy infrastructure across the Persian Gulf. The move has sent shockwaves through global energy markets, with crude oil and LNG futures surging on international exchanges.

Impact on Global LNG Markets

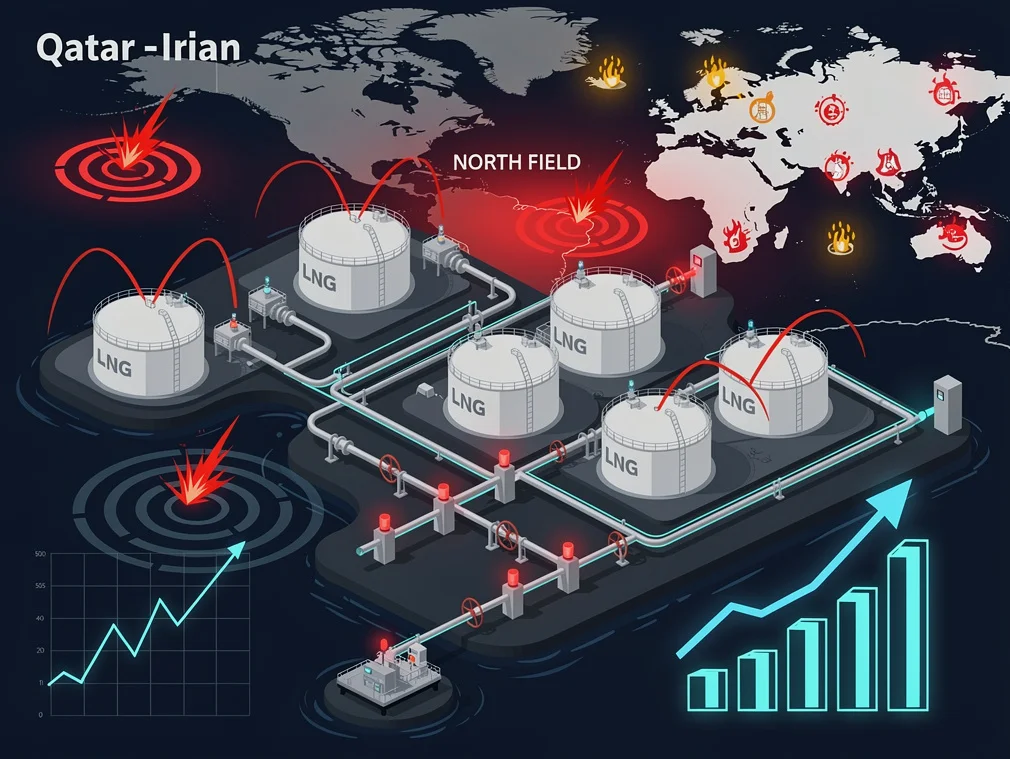

The strikes reportedly affected facilities connected to Qatar’s North Field, the largest non-associated natural gas field in the world. The North Field, which Qatar shares with Iran (where it is known as the South Pars field), contains estimated recoverable reserves exceeding 900 trillion cubic feet of gas. QatarEnergy had been in the midst of a massive expansion project, the North Field Expansion, designed to increase the country’s LNG production capacity from 77 million tons per annum to 126 million tons per annum by the end of the decade.

According to Business Insider, QatarEnergy confirmed the production pause in a statement, citing damage to critical infrastructure and the need to ensure the safety of personnel across its operations. The company has dispatched engineering teams to evaluate the extent of the damage, but initial reports suggest that at least two LNG processing trains sustained significant damage. Loading operations at Ras Laffan Industrial City, the nerve center of Qatar’s hydrocarbon exports, have been suspended indefinitely.

Global Energy Markets React With Alarm

The immediate market reaction was severe. Brent crude futures jumped more than 8% in early trading following news of the strikes, while Asian LNG spot prices spiked to levels not seen since the European energy crisis of 2022. European natural gas benchmarks, including the Dutch TTF, surged as traders scrambled to assess the potential duration of the outage and its implications for supply contracts that underpin heating and electricity generation across the continent.

Energy analysts have warned that even a temporary disruption of Qatari LNG exports could have cascading effects. Qatar supplies roughly 20% of the global LNG market, with long-term contracts serving buyers in Japan, South Korea, China, India, and several European nations that pivoted away from Russian pipeline gas after Moscow’s invasion of Ukraine. “There is no spare LNG capacity sitting idle that can replace Qatari volumes overnight,” one London-based commodities strategist told reporters. “This is the kind of supply shock that reprices the entire forward curve.”

Geopolitical Tensions Escalate

The Iranian strikes did not occur in a vacuum. Tensions between Tehran and several Gulf states have been escalating over a constellation of issues, including disputes over maritime boundaries, nuclear program negotiations that have stalled repeatedly, and proxy conflicts across the Middle East. Iran’s decision to target energy infrastructure — a move that risks drawing in major global powers with direct economic stakes in Gulf energy flows — signals a willingness to escalate that has alarmed diplomats and defense officials across multiple capitals.

Qatar has historically maintained a more conciliatory posture toward Iran than some of its Gulf Cooperation Council neighbors, in part because the two countries share the massive gas field that is the backbone of Qatar’s economy. That shared resource has served as a kind of mutual deterrent, making direct conflict between the two nations economically irrational for both sides. The strikes suggest that calculus may have shifted in Tehran, or that internal political dynamics within Iran’s leadership have overridden economic pragmatism.

The United States, which maintains its largest Middle Eastern military installation at Al Udeid Air Base in Qatar, has condemned the strikes and signaled that it is consulting with allies on an appropriate response. The U.S. Fifth Fleet, headquartered in nearby Bahrain, has reportedly increased patrols in the Strait of Hormuz, the narrow chokepoint through which roughly 20% of the world’s oil supply passes daily. Any further escalation that threatens freedom of navigation through the strait would compound an already dire energy supply situation.

Insurance and Shipping Industry Concerns

Beyond the direct impact on gas production, the strikes have triggered a reassessment of risk premiums across the Persian Gulf shipping and insurance industries. War risk insurance rates for vessels transiting the Gulf have spiked, and several major shipping companies have reportedly paused or rerouted LNG tanker movements pending clarity on the security situation. The cost of chartering LNG carriers, already elevated due to tight vessel availability, has climbed further as the market prices in potential delays and diversions.

The financial impact on QatarEnergy itself could be substantial, though the state-owned company has deep reserves and the backing of one of the world’s wealthiest sovereign wealth funds, the Qatar Investment Authority. Analysts estimate that each day of full production stoppage costs QatarEnergy hundreds of millions of dollars in lost revenue, based on current LNG prices and contracted volumes. The company’s expansion partners — including Shell, TotalEnergies, ExxonMobil, ConocoPhillips, and Eni — face their own financial exposure and will be closely monitoring the situation.

The critical question now is how long the production halt will last. If QatarEnergy can restore operations within days, the market impact, while painful, may prove manageable. A disruption lasting weeks or months, however, would force buyers to compete aggressively for limited alternative supplies, driving prices sharply higher and potentially triggering demand destruction in price-sensitive markets across South and Southeast Asia.

Alternative LNG suppliers, including the United States, Australia, and a handful of smaller producers in West Africa and Southeast Asia, are already operating near capacity. U.S. LNG export terminals along the Gulf of Mexico coast have been running at high utilization rates, and while some incremental volumes could be redirected from lower-priority buyers, the scale of potential Qatari shortfalls dwarfs available swing capacity. Australia’s major LNG projects in Western Australia and Queensland face their own maintenance schedules and contractual obligations that limit flexibility.

Comments

No comments yet

Be the first to share your thoughts